BLOG. 3 min read

April 20 marked a new event in the history of crude oil prices when the WTI May futures that were about to expire the next day traded in the negative territory at a historic low of -$37.63. This was the result of a very low demand for oil as the global lockdowns to mitigate the effects of the pandemic brought economic activity to a standstill. This in turn resulted in a huge surplus of oil that has left oil producers and traders scrambling for storage. The fear is that, if forced to accept delivery of crude oil upon the futures expiration, it would leave the party with the long position of having nowhere to store it, as the excess supply has already filled up the storage tankers across the US. This explains the negative May futures price.

A number of our commodity clients and financial institutions with commodity exposures are affected by this behavior. Those clients are actively discussing alternative modeling approaches with us as they endeavor to ensure that their risk management framework is able to handle negative commodity future prices. There are two main aspects that need consideration from a risk management perspective:

- Monte Carlo scenario generation to calculate VaR

- Option pricing

A standard approach taken by our clients to model commodity forward curve behavior for Monte Carlo scenario generation is to utilize Algorithmics’ Commodity Forward Curve (CFC) model, which is an extension of GBM that incorporates the increasing volatility of a contract as it gets closer to maturity using roll schedules. However, GBM which is a lognormal model therefore it assumes positive underlying risk factor values and cannot handle the negative future price environment.

The alternative models that clients consider (and that are fully supported in our solution) are Normal and Shifted Lognormal (SLN) Models. The normal model would produce large negative prices with a higher probability given the high volatility in the oil prices, which may not be the desired behavior based on the observed oil price dynamics. The other approach, shifted lognormal model, will produce scenarios comparable to a lognormal model, where a shift is applied to the risk factor data to ensure positive prices before generating the scenarios. The shifted risk factor data will continue to hold the same variance and covariance characteristics as the original data, and the SLN model will continue to produce the log normally distributed scenarios as expected.

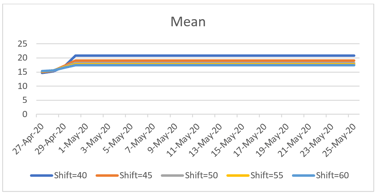

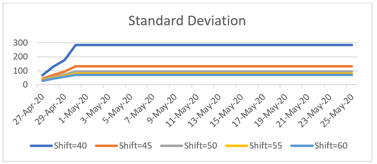

The choice of shift will have an impact on the distribution of the generated scenarios. The shift should be at least equal to the minimum negative price observed for a given risk factor to ensure the shifted risk factor values are positive to allow modeling using the lognormal model. A choice can be made between applying the shift to a single prompt contract—for example, the first prompt—vs. applying the shift to the full forward curve. The following graphs represent the scenario statistics of multiple simulations with different shift amounts using the SLN model. The analysis is performed as of April 24, 2020, utilizing 3 months of time series data that includes the negative price observation. Forward-looking scenarios were generated for a period of 1 month.

Scenario statistics for WTI promptness1 modeled using Shifted lognormal model with multiple shift amounts

Our clients are also actively revisiting their modeling approach to pricing various commodity options including European, American and Asian options and exploring alternate modeling choices such as Shifted Lognormal and Bachelier models to account for potential negative future prices. SS&C Algorithmics is actively collaborating with our clients to support their modeling needs around scenario generation and pricing in these unprecedented times. Our clients need risk solutions that overlay powerful pricing and scenario generation engines are designed to be flexible and support the evolving market conditions at a fast pace.

In these unusual times, it is hard to cover every eventuality. Maybe the oil price turning negative was a one-off event? Or maybe it was a blueprint for other commodities or other factors to go negative in the future. Either way, risk management solutions cannot afford to ignore these trends, or find a "workaround" for them; systems need to be robust, now more than ever before.

For further information about SS&C Algorithmics solutions, please visit our product page.