BLOG. 4 min read

Like a hurricane that never ends, the investment management industry continues to be buffeted by disruptive forces – fee compression, technology, regulatory uncertainty, the list goes on. To that end, we recently surveyed Heads of Product Management and Product Development from 35 firms across the industry to get their perspectives on key issues. We also sat down with approximately 15 product leaders for a discussion of the key issues affecting them and what we heard was very interesting. No surprise, it is the ‘lack of asset growth’ combined with ‘platform rationalization’ that is driving fund closures, with approximately 75% of the firms we surveyed closing funds in 2018 and 80% planning to close funds in 2019.

Although there is a large degree of institutional inertia behind keeping funds open, whether due to the belief that a particular strategy will one day be in favor or portfolio managers with a keen interest in a certain fund, it seems clear that the tide has turned against keeping funds open as a form of optionality. Additionally, price cuts continue with some 75% of firms planning to cut prices on selective products. Most recently, a major firm announced that it is cutting fees on a large number of its funds, and on an annualized basis we calculated that the hit to revenue from the closure of the first eleven funds was just over $25 million. Needless to say, these types of cuts are not unsubstantial and they present a large challenge to those managers looking to gather assets and drive revenue growth. We see no end in sight and continue to believe that the industry will remain challenged through the rest of 2019 and into 2020.

However, in spite of industry challenges, we are confident that asset managers will continue to innovate with new investment strategies and product structures. For example, we continue to see new Environment, Social and Governance (ESG) products as ESG becomes increasingly mainstream and moves beyond just equities into fixed income and even money market funds. A number of firms have indicated interest in bringing strategies to the market, and in fact, when we asked firms to rank the top five product launch priorities over the next 12 months, ESG strategies ranked #2 on a weighted basis while multi-asset model portfolios were #1. Morningstar reported that there were 351 sustainable US mutual funds and ETFs at the end of 2018, up almost 50% from 2017. In fact, we believe ESG funds are likely to continue to take in record amounts of net new money, even as the overall industry struggles.

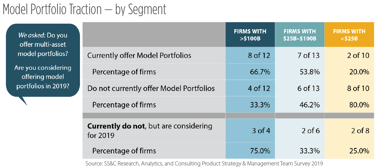

In regard to model portfolios, there was a clear distinction among firms when delineating by size, with larger firms expressing a much more definite intent to launch model portfolios. Larger firms are manufacturing these products as both a complement and a competitor to in-house models offered by distributors. In our opinion, it seems likely smaller firms have evaluated the market and decided that they do not have the scale to successfully compete in this space. Rather, they will concentrate on bringing best-in-class products to markets that can be used in a ‘plug and play’ manner with third party models. Conversely, larger firms that have operational scale and are increasingly desperate for new revenue see models as a source of potential growth driven by packaging existing mutual funds into new wrappers using already well-developed asset allocation capabilities.

Going forward there seems to be a consensus that the industry will be looking to innovate in the ETF and alternative space. The SEC’s recent decision to approve Precidian’s non-transparent active ETF methodology will likely result in a wave of new funds in 2020 as traditional active managers take advantage of a new product wrapper. While this will present challenges for product development teams at investment managers, as well as due diligence teams at broker dealers, it will be interesting to see if the availability of previously unavailable strategies in an ETF wrapper acts as a true catalyst for new flows, or if they are a manufacturer-driven product that needs to be sold, or a consumer demand-driven product to be bought. Similarly, interval funds (which typically provide limited quarterly liquidity) have been the subject of interest at a number of firms, and there are a wide variety of these products in the pipeline to be launched. Also on the radar screen is a potentially new product structure which we discussed in our meeting with product heads—a so-called Auction Fund, which is being marketed by NASDAQ Private Markets. While still in the very early days, given the roughly 50% decline of U.S.-listed public companies in the last 20 years and the increasing number of investment opportunities outside public markets, it seems apparent that the industry needs to find a structure that will provide access to investments outside the traditional public markets. Auction funds are, for all intents and purposes, privately placed versions of exchange-traded funds for illiquid assets with a market auction instead of a redemption or tender back to the fund, with a series of mechanisms to keep the auction pricing near the net asset value. One industry participant calls them slow motion ETFs. As such, they may provide access to illiquid investments to a much wider group of investors who require liquidity, and perhaps even allow 401(k) plans to more broadly incorporate these investments. Good examples of the type of investors that might make use of these non-correlated investments are the in-house models constructed by distributors, where the ability to rebalance between various asset classes is viewed as integral.

On a final note, while it is clear that the industry is struggling to adjust to a new world, the pool of investable capital continues to increase—not just in the US, but around the world. At the same time, solutions and/or outcome-oriented investments will be increasingly required to meet the needs of an aging population that is increasingly bearing the burden of preparing for a future in which the government and employers cannot be relied upon. How firms respond to this challenge—i.e. their ability to deliver consistent alpha in a variety of structures (mutual funds, active ETFs, CITs, model SMAs)—will determine whether they succeed or not. In this world, the role of Product Management and Product Development teams will be critical. Our research indicates that they are actively preparing for this challenge.

Related articles

BLOGS. March 8, 2019

ETFs – Looking Into the Future: A Recap of the Annual Inside ETF Conference

Read more

BLOGS. May 3, 2019

Active Non-Transparent ETFs and Mutual Funds – A Transformational Change?

Read more