BLOG. 3 min read

The expectations and scope of financial advice have evolved considerably over the past 10 years. Meanwhile, growing wealth and slow growth in the number of financial advisors in the industry represent increasing opportunities for existing and new financial advisors to grow their practices. As a result, what advisors are looking for from their asset management partners continues to change.

The average age of financial advisors has been rising as fewer graduates opt to go down that route, citing reasons from lackluster pay compared to other jobs in the field to difficulty of the certification exams to the reputation of the field as a whole, among others. Out of the 83,000 CFPs in the industry, there are more CFPs over 70 than under 30 and, around 40% of financial advisors plan to retire over the next 10 years. This leads to the forecast of there being 6% fewer financial advisors by 2022 compared to 2017.

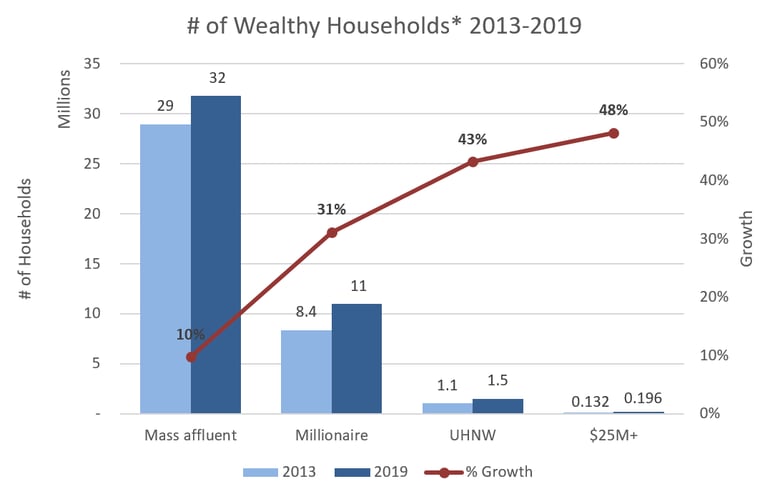

Meanwhile, in 2019, and for the 10th consecutive year, the number of wealthy households* in the US reached a record high. The number of mass affluent households increased by 10% from 2013 to 2019, reaching 32 million households. Of these mass affluent households, 69% have a financial advisor—a lower proportion than the millionaire (75%) and ultra-high net worth (81%) households. In all three segments, however, there is a sizable number of households—representing a considerable amount of wealth—not receiving financial advice.

* Mass affluent: $100,000 - $1 million

Millionaires: $1 million - $5 million

Ultra High Net Worth: $5 million - $25 million

With fewer advisors and the addressable market continuing to grow, financial advisors find themselves with larger books of business and more opportunity. Coupled with this, the rise and adoption of technology and greater availability of information mean that clients expect their financial advisor to offer a comprehensive approach to fulfill most, if not all, of their financial needs. Financial advisors now find themselves needing to be knowledgeable in matters like healthcare planning, divorce, college planning and admissions, behavioral finance, housing loans, startups and small businesses, and the list goes on. Financial advisors have turned to technology, team-based approaches and third-party services to help meet these expectations. Many of the functions that used to take up a considerable part of an advisor’s time, like reporting, investment monitoring and portfolio rebalancing, are now automated. Third-party or in-house models have replaced portfolio design in many instances. Advisors are now able to spend more time meeting with clients and catering to the types of needs mentioned above—either themselves or through partners that they work with.

From an asset manager’s perspective, this means that what an advisor requires from their firm has also changed. Similar to financial advisors’ relationships with their clients, their relationships with asset managers have become a more nuanced one that is focused on helping them manage their business and address their increasing demands. Previously, an advisor would mainly have a relationship with a firm’s wholesaler. They would meet with that wholesaler periodically and would rely on them to facilitate and provide any information and resources they needed. They would often inquire about fund facts, the portfolio manager’s investment approach, product risk profile, etc. Today, an advisor’s interaction with an asset manager is increasingly fluid and spans a wider range of topics communicated through numerous touchpoints. They may visit a firm’s website for information, receive emails and product materials through marketing campaigns, attend a firm’s webinars, and view the firm’s information on third-party platforms such as LinkedIn and Morningstar.

An advisor should receive the same messaging across all of these touchpoints, and it should be shaped by previous interactions with the firm. Some things to ask include:

- How many times have they visited your website and what did they view?

- Which emails did they open?

- Which articles did they read on third-party platforms?

- Which products did they reach out to your firm about?

- Which webinars did they attend and what questions did they ask?

- How often do they prefer to meet and how (virtual/in-person/phone)?

- What concerns did they express during meetings?

The answers to all of these should be captured and systematically used to tailor future communication and interaction with the advisor. Capturing and acting upon what can end up being an exceedingly large amount of information requires robust data management capabilities on the part of asset managers. Business intelligence, sales, marketing and product teams must work together to ensure the data infrastructure is designed, maintained and populated efficiently and accurately. Needless to say, any content that is created within the firm should be geared towards addressing the concerns and meeting the business needs that advisors are communicating through the touchpoints above. The more seamless and homogenous this experience is, the more it will facilitate a more meaningful, mutually beneficial relationship with advisors, leading to higher satisfaction and the likelihood that they will continue to do business with your firm.

For more on SS&C’s data management capabilities, contact us.