BLOG. 6 min read

The Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC), On April 20, 2026, issued a joint proposal that marks a substantial evolution in the regulatory landscape for private funds, necessitating significant adjustments in reporting methodologies and data granularity.

The proposal follows a period of significant regulatory uncertainty concerning Form PF. Form PF is the confidential reporting form for certain SEC-registered investment advisers to private funds, including those also registered with the CFTC. Rather than implement the extensive 2024 amendments, regulators have elected to pursue a revision and simplification intended to alleviate regulatory burdens while maintaining the collection of essential systemic risk data, with the goal of “significantly reducing burdens for advisers required to file Form PF.”

The most immediate impact of the proposal will be felt by small to mid-sized managers, who will see their reporting burdens effectively erased or dramatically reduced.

-

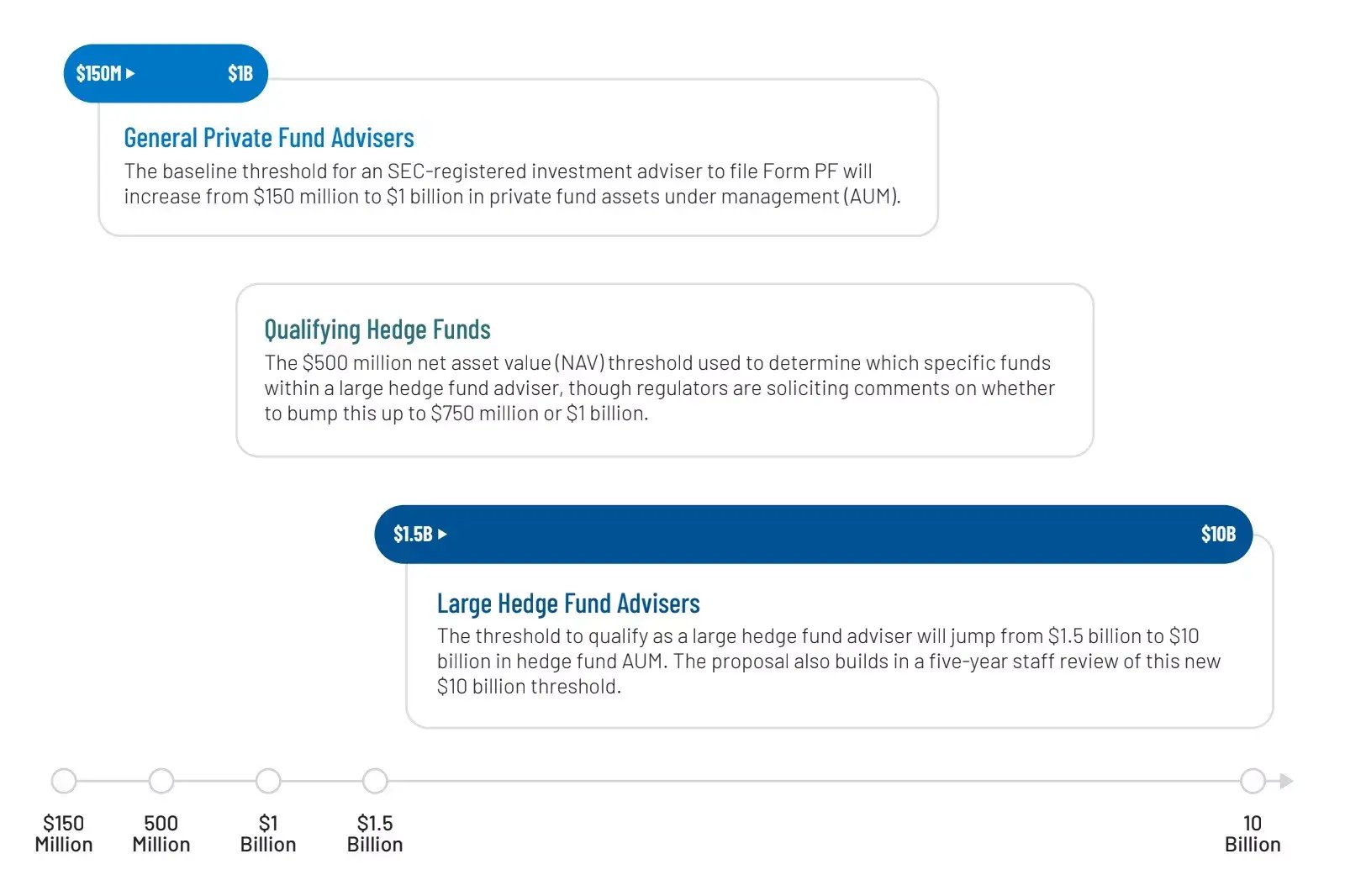

General Private Fund Advisers: The baseline threshold for an SEC-registered investment adviser to file Form PF will increase from $150 million to $1 billion in private fund assets under management (AUM).

-

Large Hedge Fund Advisers: The threshold to qualify as a large hedge fund adviser will jump from $1.5 billion to $10 billion in hedge fund AUM. The proposal also builds in a five-year staff review of this new $10 billion threshold.

-

Qualifying Hedge Funds: The $500 million net asset value (NAV) threshold used to determine which specific funds within a large hedge fund adviser qualify, though regulators are soliciting comments on whether to bump this up to $750 million or $1 billion.

In comparison to the current form, the structure of the proposed form itself has undergone modifications, with the elimination of the distinction between Sections 2a and 2b.

The proposal introduces a comprehensive set of new data points, encompassing NAICS codes, adjusted exposures and detailed breakdowns of investor classifications, borrowings and counterparty exposures.

Additional reporting requirements include GAV/NAV for all three reporting months, unfunded commitments, contributions, withdrawals, expanded investor classifications, IRR and new strategies such as digital assets. These enhancements are intended to provide regulators with a more granular and comprehensive overview of the private fund industry.

The structure of counterparty exposures and borrowings questions has been revamped, and interest rate derivatives are now categorized separately with dollar value reporting for trading and clearing questions. Also, new questions demand exposure reporting based on currencies, countries and sectors.

The proposal also introduces significant changes to static data requirements. Funds will now be required to disclose their registration status as a CPO or CTA, as well as their fund type, including commodity pool, UCITS, AIF or money market fund.

The form also requires specific details about trading vehicles, including legal name, LEI and RSSD ID, as well as the nature of the fund's involvement with the trading vehicle. Additionally, open-ended and closed-ended funds must provide specific information about their structure and redemption terms, while feeder funds must disclose details about their master fund investment.

Collectively, these enhancements aim to provide regulators with a more comprehensive, granular and risk-sensitive dataset, facilitating a deeper understanding of the private fund industry and enabling more effective oversight.

Borrowings and Counterparty Exposures

- The proposal streamlines reporting by consolidating counterparty risk into one section, replacing earlier questions (22, 23, 36, 37, 43, 45) with more detailed disclosures on exposures, collateral and borrowing. Question 26 (in the proposal) expands scope to include borrowings, collateral posted, lending and collateral received. The earlier percentage split of borrowings (US vs non-US, financial vs non-financial) has been removed. The counterparty exposure table now requires separate reporting for CCP and non-CCP cleared derivatives, including mark-to-market exposures, gross notional values (for non-CCP), and both cash and securities collateral.

- Questions 27/42 require identification of creditors for cash borrowings (pre-collateral), while 28/43 cover counterparties with net mark-to-market exposure (post-collateral).

Currency, Country and Sector Exposures

- The proposal requires funds to report long and short positions across currencies, including both direct holdings and indirect exposures from foreign assets and derivatives, to assess exchange rate risk. Only exposures above set thresholds must be disclosed. Question 33 mandates monthly reporting, split into two parts: a topline summary of total long and short exposures from FX derivatives and foreign-denominated assets/liabilities, with positions bifurcated into long and short.

- Similar to Question 33, revised Form PF Question 35 sets thresholds for reporting country exposures. Funds must disclose exposures above the threshold using ISO country codes. Q35 aligns conceptually with Q28 of the existing Form PF.

- Question 36 requires disclosure of industry-wise exposures using NAICS codes to assess concentration risk. Exposures must be split into long and short positions, similar to Q33 and Q35. Managers can report using 2- to 6-digit NAICS codes based on a company’s primary business activity.

Asset Exposures

- Another area that sees a major change in reporting is the proposed Question 32 (Question 26 in the current form).

- The proposal introduces new sub-asset classes and an added “Instrument Type” section. It requires reporting of adjusted exposure by netting positions across instruments and includes reporting of 10-year bond equivalents separately for positions at an instrument-type level that bear interest rate risk.

Trading Activity

- Question 24 on the current form (Q29 proposed) introduces a new bucket for reporting of interest rate derivatives. Instead of a percent split between Exchange/OTC or CCP/Bilaterally in various sections, the proposal requires reporting of actual values. Question 27 (Monthly Turnover) has been eliminated.

Risk Questions

- Requirements pertaining to Value at Risk and Scenarios Testing remain unchanged.

Rationalizing Section 5 Current Reporting

- For large hedge fund advisers, subject to rapid "Current Reporting" under Section 5, the proposal brings clarity and a higher bar for triggering events:

- The timeline for filing "as soon as practicable, but no later than 72 hours" has been deleted. The standard is now "Within 72 hours," resolving interpretive uncertainty.

- Current reporting for margin defaults would be eliminated.

- Definition of "operations event" would be narrowed.

- Current reporting for inability to satisfy redemption requests would be eliminated.

Section 6 Private Equity Quarterly Event Reporting

- The proposal would eliminate Section 6 in its entirety.

- This removes quarterly reporting obligations that currently require private equity fund advisers to report adviser-led secondaries, GP removals, termination of investment periods, fund terminations and other trigger events.

Status Quo for Private Equity and Liquidity Funds

- It is worth noting that while hedge funds see massive changes, the landscape for Large Liquidity Fund Advisers and Large Private Equity Fund Advisers remains virtually static.

- The AUM thresholds remain at $1 billion and $2 billion, respectively, and all substantive content in Sections 3 and 4 is preserved.

- The only changes in these sections are minor editorial corrections regarding master-feeder reporting instructions and glossary typos.

Looking Ahead

This proposal was published in the Federal Register on April 24, 2026. Comments should be received on or before June 23, 2026.

The proposal specifically requests comment on the threshold amounts, including alternative levels of $250 million, $500 million, $2 billion, $3 billion and $4 billion for the general threshold, and $2 billion, $3 billion, $5 billion, $15 billion and $20 billion for the large hedge fund adviser threshold. If the 2026 proposal is adopted, the release establishes a transition period of at least 12 months from the date of publication in the Federal Register.

Managers should start engaging in conversations about how these changes to the current form impact them, including sourcing new data points, adoption of methodologies for computing responses to amended and newly added questions and designing a solution to implement the amendments.

Contact us to learn how SS&C can help you in this process.