BLOG. 4 min read

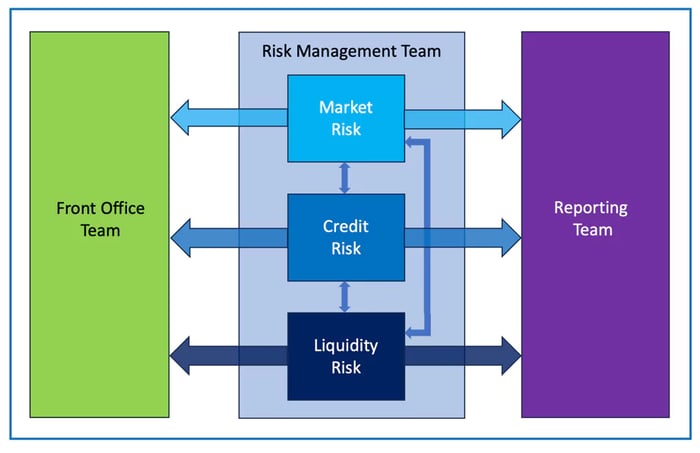

For asset management risk specialists, the ability to monitor portfolios’ integrated risks remains operationally complex and insightful to business stakeholders. Driven by organizational constraints or legacy reasons, these risk investigations are often performed in silos. Distinct tools and workflows are in place to support market, credit and liquidity risk analysis. As illustrated in Fig.1, disjointed processes seldom account for risk-type interactions. These streams may also rely upon different data sources or run at different frequencies. These factors can add inconsistencies in areas of functional overlap such as instrument pricing models or risk horizons.

Fig. 1 – Towards a more integrated risk management mind-set

The importance of evolving to a more integrated risk management approach overcomes these shortcomings and can be illustrated with a corporate bond portfolio example.

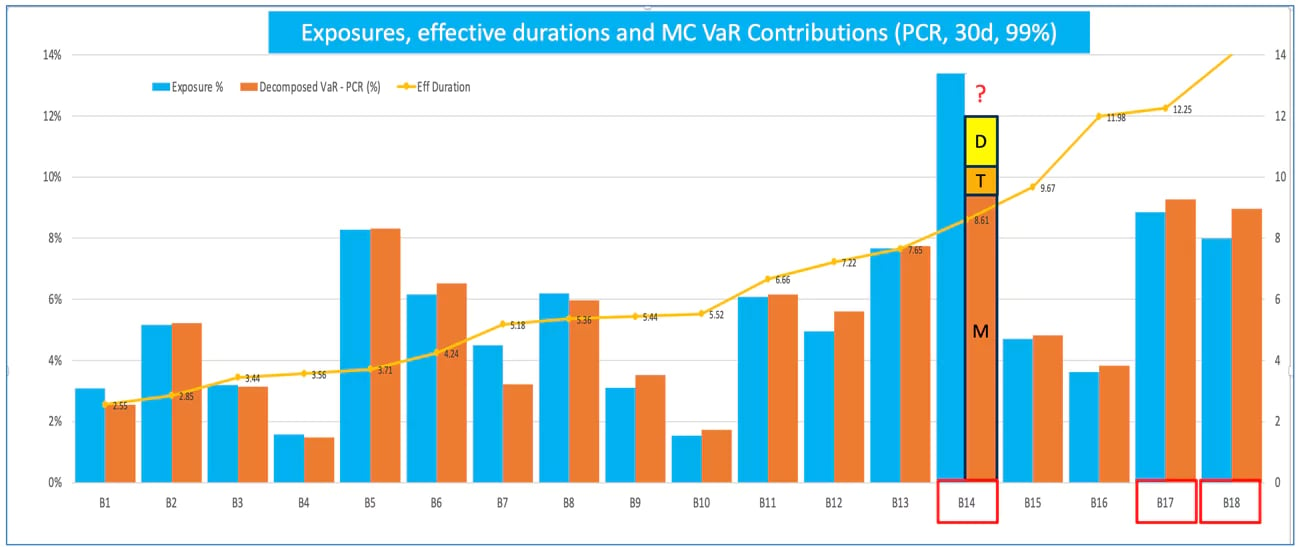

Figure 2 features a hypothetical fixed-income portfolio composed of 18 investment-grade bond positions. Holdings are labeled “B1” to “B18” in increasing effective duration order. Leveraging advanced valuation models and stochastic simulations, the fund’s risk managers can draw a clear picture of top exposure contributors (blue bars). They can also quantify bond contributions to the integrated market and credit risks of the portfolio (orange bars). In this example, accounting for market, rating migration and default risks in a single stochastic Value-At-Risk (VaR) indicator, “B14,” “B17” and “B18” are the riskiest positions.

Fig. 2 – Exposures and integrated market and credit risk contributions of individual bond portfolio holdings

The introduction of a second element, rating migrations and defaults, can change the pure market risk picture of the fund. Assuming constant positions, this picture would likely change if risk managers decided to focus on high quantile tail risk indicators (Expected Shortfall, or CVaR) instead of VaR. The picture would also change as the stochastic simulation horizons increase from 30 days to 3 months or more. Time is indeed part of the risk/return trade-off.

The third element introduced in this integrated risk management advocacy is liquidity. The monitoring of liquidity measures is now of prime importance to asset managers. Regulators around the world put a strong emphasis on the reporting of market and funding liquidity indicators across a wide range of investment fund types. For bond fund managers in particular, the integration of market liquidity considerations is linked to strategy implementation too.

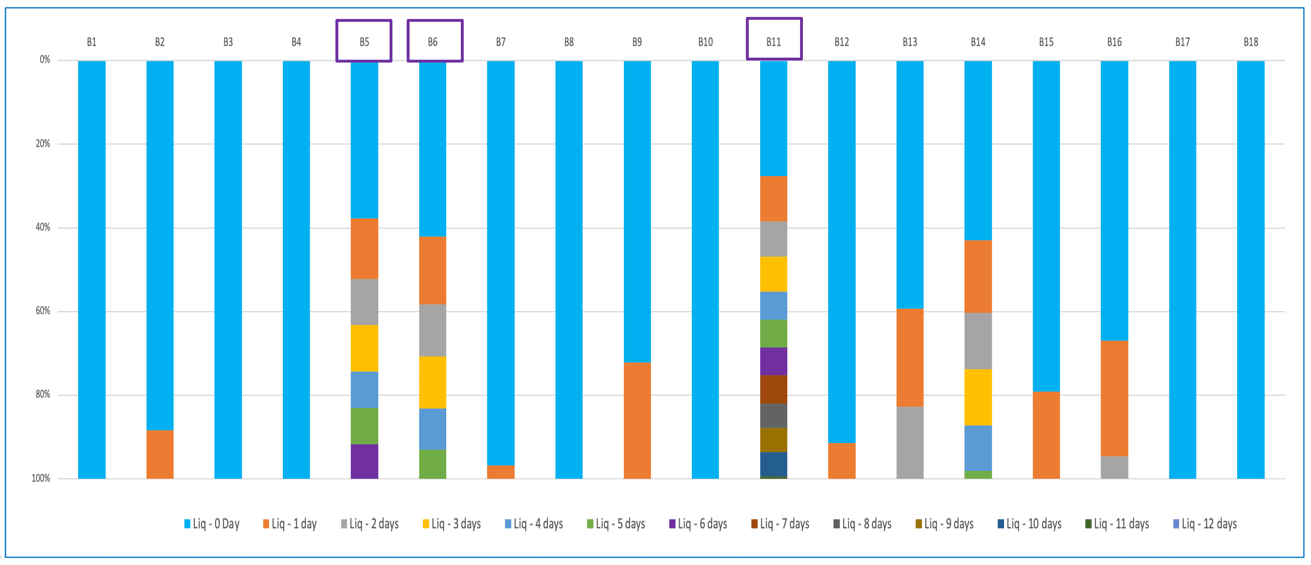

To illustrate this aspect, we extend our initial market and credit risk picture, and generate a market liquidity view of the 18-bond fund. The chart below (see Fig. 3) provides insights into the expected liquidation profile of individual positions. This analysis leverages the ICE LST data service and SS&C Algorithmics analytics. Under current market conditions and a fixed trading cost assumption (50bp), risk managers can identify “B11,” “B5” and “B6” as the hardest-to-liquidate positions in the fund. It would take respectively 12, 6 and 5 days to fully liquidate these positions under the selected modeling assumptions. Conversely, two of the top market and credit risk contributors (“B17” and “B18”) would not present any divestment challenge under this “current market; 50bp” scenario.

Fig. 3 – Expected market liquidation schedules across bond portfolio holdings (Liquidated position % vs time horizon)

Each risk specialist and investment manager can draw different portfolio rebalancing conclusions from this example. Most can agree on the added value of these extended data and risk analytics insights.

- Evolving to a more integrated risk management mindset represents an organizational and operational challenge to a lot of asset managers. However, overcoming these burdens can yield benefits through the build-up of an improved decision-making framework.

- Regulatory and financial market evolutions continue to drive investment managers’ needs for market liquidity insights. Tradeable volumes for bonds varied a lot over recent years as well. It means market liquidity data and simulation capabilities need to be part of the broader daily risk management process.

- While the largest investment teams still often operate their risk analytics platforms “in-house,” most asset managers leverage external Cloud infrastructures to support computational and data aggregation needs. For these firms, the adoption of hosted risk analytics or managed services can be effective ways of turning integrated risk management concepts into a daily reality.

To learn more about liquidity stress testing for market risk management, download our SS&C Algorithmics "Liquidity Stress Testing for Market Risk Management" research report.