BLOG. 3 min read

In part one of our blog series on ETF trends, we focused on the current state of the active ETF landscape with its outsized flows and rapid proliferation. We must recognize how we got here to better understand where we are now. In this continuation, we will look back at some of our predictions from four years ago and highlight several factors that contributed to active transparent ETFs becoming the preferred option over their semi-transparent counterparts.

In our Product Management and Development article in Product Strategy Compass four years ago, we predicted that active managers would ultimately employ active semi-transparent ETFs as the primary vehicle to offer their active capabilities to the market. Since then, adoption both by product providers and by distributors has been extremely slow. Rather, it appears that asset managers have dealt with their previous concerns that fully transparent active ETFs might in some way endanger their capacity to generate investment alpha. The growing acceptance and availability of active transparent ETFs at distributors during this time was likely a catalyst for product providers to overcome said fears.

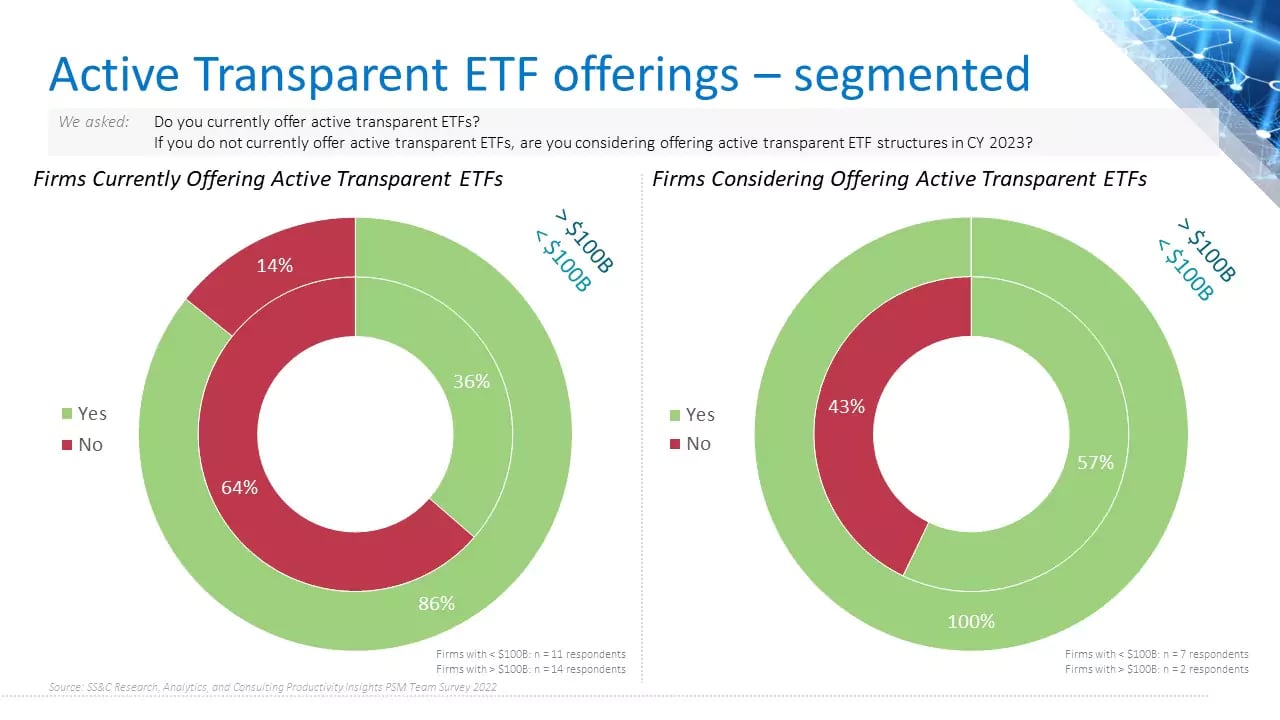

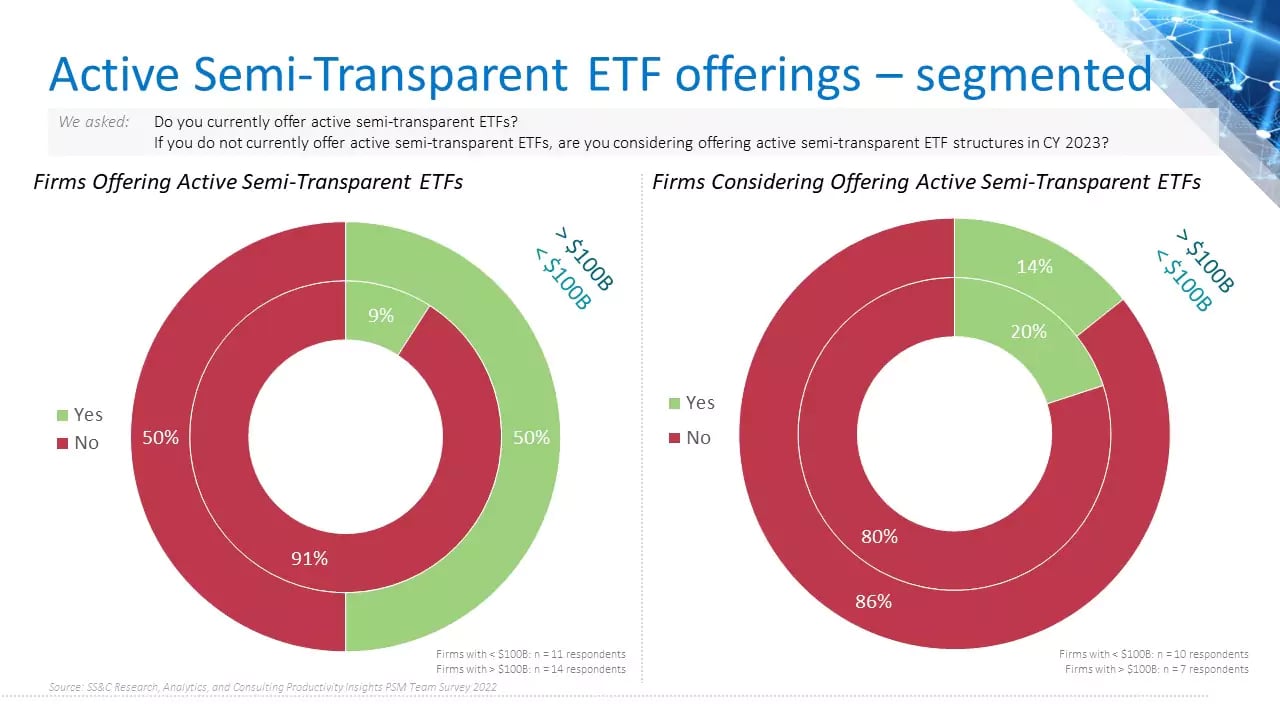

Responses from our most recent Product Strategy & Management survey regarding current and anticipated active transparent ETF offerings signaled an overwhelming appetite for the structure as 88% of firms either currently offer active transparent ETFs (64%) or are considering offering their first in 2023 (24%). When asked the same set of questions about active semi-transparent ETF structures, the interest from product heads was considerably muted by comparison, with just 32% of firms currently offering active semi-transparent ETFs. Moreover, managers who have yet to utilize active semi-transparent ETFs do not appear inclined to adopt them in the future, as only 18% of those firms that do not currently offer the structure are considering offering their first in 2023. Sparse adoption from providers aligns with the industry's bearish view regarding the structure's asset-raising potential as 50% of respondents are of the opinion that the potential for active semi-transparent ETFs in the near-, medium-, and long-term future is limited at best and non-existent at worst.

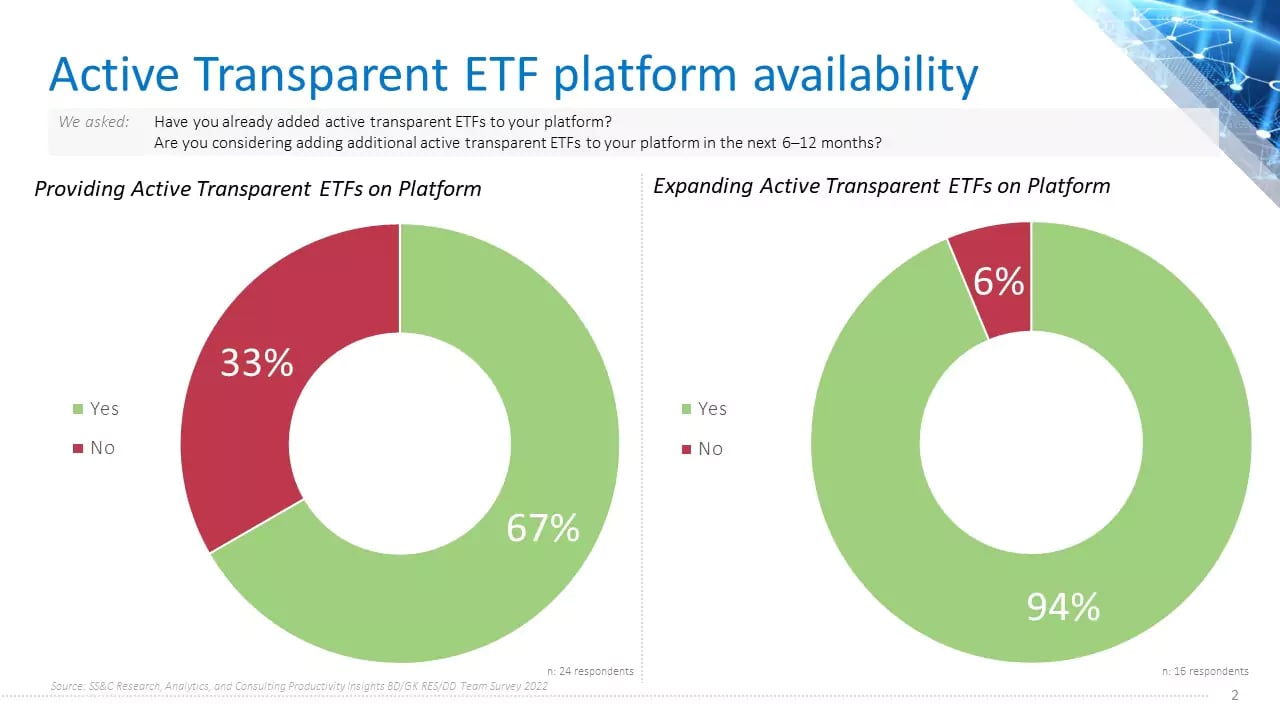

Our canvassing of distributors' due diligence teams regarding their usage of and plans for transparent and semi-transparent actively managed ETFs revealed a penchant for fully transparent active ETFs over their semi-transparent peers, echoing findings from the survey of product management teams. Active transparent ETFs are currently available on 67% of distributors' platforms with the number of these ETFs available on platforms set to grow rapidly as 94% of distributors offering active transparent ETFs are considering adding more to the platform in 2023. The support and interest in active semi-transparent ETFs amongst due diligence teams' is not nearly as robust as 63% of distributors do not have a single active semi-transparent ETF available on the platform. Moreover, 80% of distributors who have not yet added active semi-transparent ETFs have no apparent interest in providing them on the platform in 2023. With shelf space at less than half the distributors and a very limited pool of potential new entrants waiting in the wings, the rate of adoption for active semi-transparent ETFs will remain conservative.

While industry adoption of active transparent ETFs has flourished recently, widespread adoption of active semi-transparent ETFs has been impeded greatly by several substantial lingering obstacles. We asked distributors and managers what they believed to be the single biggest hurdle facing active semi-transparent ETFs and, as expected, a large number pointed to the lack of demand/shelf space, securities restrictions, lagging education, regularity complications and tax efficiency concerns. Looking beyond the predictable talking points, there were a few hurdles mentioned by multiple respondents in each survey:

- Semi-transparent ETFs solve a manager problem, not a client problem.

- Increases burden for due diligence professionals' decision-making processes.

- Investors want and have become accustomed to transparency.

- Quantity of high-quality transparent offerings available.

An underlying theme from many of the distributors' and managers' responses was that the longer-term viability of the semi-transparent ETFs is uncertain as the adoption, availability, activity and flows into fully transparent strategies will only exacerbate the considerable headwinds facing the structure.

Stay tuned for part three of my ETF-focused blog posts, which will examine active ETFs' significant sway over managers' product and business priorities. And suppose your firm is working on its ETF strategy. In that case, SS&C’s Distribution Solutions group focuses on helping asset management firms find opportunity amidst all of the disruptions in the industry, as well as helping them stay on top of industry trends.