Tags

Robert Dean

Principal Technical Manager, Pensions & Actuarial Services

July 5, 2019

6 min read

Previously, we’ve written about the benefits and challenges associated the new GMP legislation. Let’s look at how calculations would play out in a real-world example.

Our Scheme member:

- Mrs. Oswald

- Date of Birth - 12 March 1964; Age 55

- Service Dates

- Pre-Barber 3 Nov 1989 to 16 May 1990

- Equalisation period 17 May 1990 to 5 Apr 1997

- Post-GMP service 6 Apr 1997 to 14 Sep 1998

- Salary at date of leaving: £20,000 p.a. (from Apr 1998)

Why do inequalities arise?

Male members accrue GMP at a faster rate, so a male member with the same service dates as Mrs. Oswald would have a lower GMP. The total pension at date of leaving service will be the same, but the proportion that represents GMP will differ.

GMP will be put into payment from age 60 for Mrs. Oswald. The male equivalent member would have GMP put into payment from age 65.

As schemes treat GMP and non-GMP differently when it comes to revaluation, increases and spouses benefits, various inequalities arise. There are also various statutory checks that will be impacted by the difference in the GMP proportions and the differences in the age at which GMP comes into payment between the sexes.

Based on a 60ths accrual and a final pensionable salary defined as the earnings received over the 12 months prior to leaving, we have a pension as at 14th Sep 1998 of £2,142.70 p.a.

Pre-GMP equalisation the pension is made up of the following component parts:

Now we repeat the calculation except we assume Mrs. Oswald is male. As before, the pension at date leaving service totalled £2,142.70 p.a. but the proportion that was GMP decreases for the middle period. This gives a pension of:

The temptation is to value the difference between the benefits for the 17th May 1990 to 5th Apr 1997 only. After all, when we look at the figures above we can see that it is only this middle period where the figures differ at date of leaving. However, we must consider the pre-97 pension as a whole, as during retirement there could well be an interaction between the GMP earned in the first period and the pre-97 Excess earned in the second and vice versa.

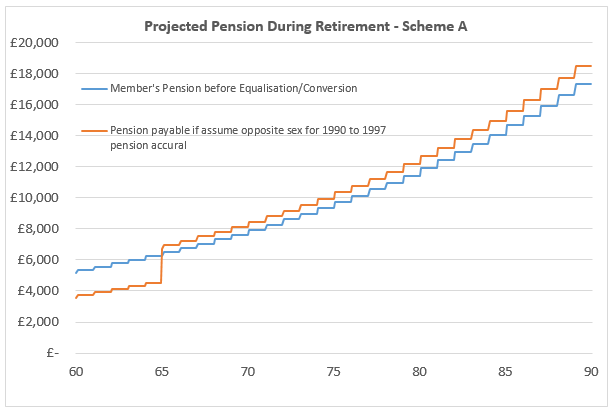

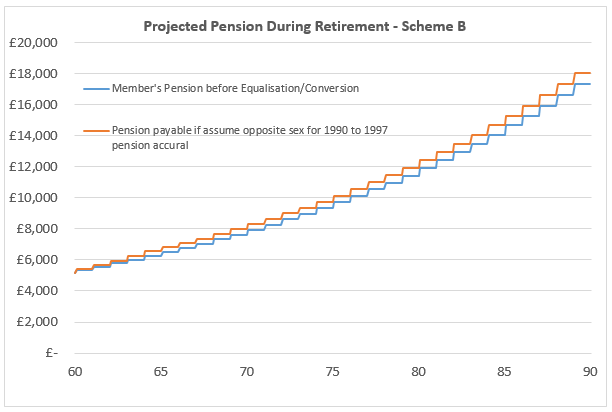

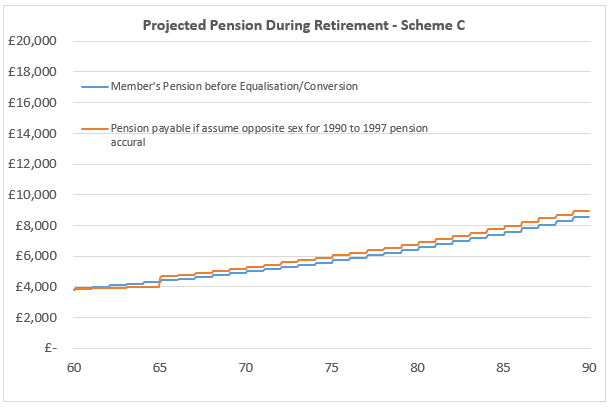

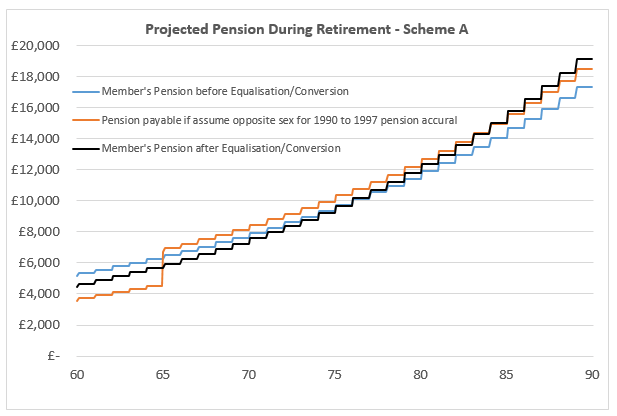

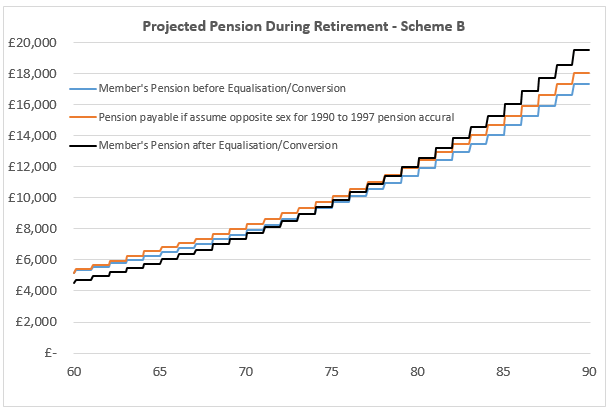

Using the example above, we have determined the benefits payable during retirement for three defined benefit schemes. For each scheme, we show the position before and after GMP equalisation.

While there is no such thing as a typical defined benefit scheme, the three schemes chosen are not uncommon. In our examples, each scheme adopts a combination of Fixed Rate GMP revaluation & Statutory non-GMP revaluation. Each provides 5% p.a. increases in payment on post-97 pension and GMP increases of CPI, subject to a maximum of 3%. All have a normal retirement age of 60 but reduce the benefits accrued in the Pre-Barber period by 30% if taken at NRD. Our three schemes have then taken different approaches in their treatment of GMP and the increases they apply to the pre-97 excess pension as follows:

Scheme A Pension at age 60 is the sum of the GMP at date of leaving plus the non-GMP revalued to 60. Revaluation on the GMP is put into payment from the members GMP Age (65 for males, 60 for females). This being similar to the example shown in the DWP’s ‘Guidance on the use of the Guaranteed Minimum Pension (GMP) conversion legislation’.

5% p.a. pension increase on pre-97 pension in excess of GMP

Scheme B Pension at age 60 is the sum of the GMP revalued to 60 and the non-GMP revalued to 60. For male members, a step is payable at GMP age only if required by legislation.

5% p.a. pension increase on pre-97 pension in excess of GMP

Scheme C Pension at age 60 is the determined as the whole pension at date leaving revalued in line with statutory revaluation. At GMP age the total pension payable is unchanged (unless it is below the revalued GMP) but the part that relates to GMP will start to receive the lower increases in payment.

No pension increase on pre-97 pension in excess of GMP

The pension cash flows for our female member and for the same member (but assuming opposite sex for the period between May 1990 and April 1997) are shown in the graphs below:

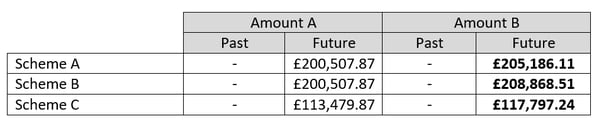

The guidance defines the value of the pre-1997 benefits before and after GMP equalisation as Amount A and Amount B respectively. To aid later discussion we have split both these values into that which relates to past benefits already paid prior to the conversion date, and that which relates to benefits due after the conversion date. The value of the past benefits being derived using Method C2, i.e. the past payments accumulated to the conversion date using simple interest of bank base rates plus 1%. The value of future benefits have been calculated using Method D—in this case adopting the same financial and demographic assumptions as prescribed by the FCA for calculating redress for defined benefit complaints (although these assumptions are parametrized in our calculation software so the scheme Actuary would be free to adopt their own basis for the Method D valuation).

We start by looking at the simplest scenario: a conversion date prior to Mr. Oswald’s retirement.

We have adopted a post-conversion pension with revaluation and increases in line with the scheme’s current practice for pre-97 excess benefits. Giving post-conversion benefits (quoted as a date of leaving) of:

For all our example schemes, the starting pension at age 60 is dependent on the actual level of CPI between now and age 60. However, for schemes A & B prior to conversion, the amount payable at retirement was made up of fixed rate revaluation on the GMP with only the non-GMP dependent on the level of future CPI. This does of course mean that if our valuation has overestimated the allowance for future CPI, then the starting pension could be less than Mrs. Oswald’s pre-conversion pension.

If future CPI is in line with the assumed rate used in the valuation basis, then the post-GMP equalisation/post-conversion pension from retirement would be as follows:

For scheme C, the member should see an initial uplift in their starting pension. However, for scheme A and B, the initial pension from age 60 will probably be lower than that which would have been paid prior to the conversion. It is true that during retirement the pension increases will be higher, as previously the pension relating to the GMP increased at CPI, max 3%pa, and now the whole pension is increasing at 5%p.a. But many members may not consider the higher increases in payment to be adequate compensation for the lower initial pension. The guidance suggests that in such circumstances the scheme may wish to consider offering alternative formats for the converted pension.

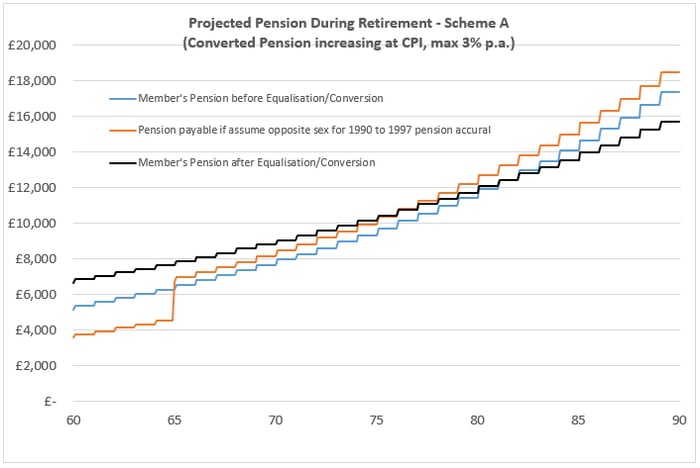

For example, if scheme A were to offer a converted pension increasing in payment line with CPI, max 3% p.a., then the initial pension should increase following the conversion exercise.

Retirement and Death cases

The Barber judgment dates back to 17th May 1990, some 29 years ago. It is of course likely that a high proportion of members who were accruing benefits in the early 1990s have since retired and/or died. In our last blog of this series, we will take a look at some of the issues facing scheme actuaries dealing with this cohort of members.

.jpg?width=355&name=shutterstock_2118854732%20(1).jpg)