BLOG. 24 min read

In the last of our GMP equalization blog series, we take a look at members who have retired and started to draw their scheme pension. We also look briefly at cases where the scheme member has died and the member’s widow/widower is in receipt of a spouse’s pension from the scheme.

Retirement cases

Similar to the previous post in this series, let’s look at how calculations would play out in some real-world examples:

Our Scheme member:

- Mrs. Atkins

- Date of birth - 12th March 1953; age 66

- Service dates

- Pre-Barber 3rd Nov 1989 to 16th May 1990

- Equalization period 17th May 1990 to 5th Apr 1997

- Post-GMP service 6th Apr 1997 to 14th Sep 1998

- Salary at date of leaving: £20,000 p.a. (from Apr 1998)

- Spouse: Mr. Atkins, date of birth - 12th March 1950; age 69

Mrs. Atkins was a member of Scheme A and started to draw her scheme pension from age 60. The scheme benefits can be summarized as:

Scheme A Pension at age 60 is the sum of the GMP at date of leaving plus the non-GMP revalued to 60. Revaluation on the GMP is put into payment from the members GMP Age (65 for males, 60 for females). This is similar to the example shown in the DWP’s ‘Guidance on the use of the Guaranteed Minimum Pension (GMP) conversion legislation.’

5% p.a. pension increase on pre-97 pension in excess of GMP

On death after retirement, the spouse receives a 50% pension

Why do inequalities arise?

The situation is largely the same as our previous example. Our member is a female with GMP accrual during the period 17th May 1990 to 5th April 1997. For this period a female member would accrue GMP at a faster rate, so an equivalent male member with the same service dates as Mrs. Atkins would have a lower GMP.

The tables below show the pension at date of leaving and at date of retirement for Mrs. Atkins. The second set of tables show the post-GMP equalization position assuming Mrs. Atkins was male for the purposes of determining the benefits accrued between 17th May 1990 and 5th April 1997.

|

Pre-GMP equalization, the pension at date of leaving is made up of the following component parts:

The scheme adopts Fixed Rate GMP revaluation along with Statutory revaluation for non GMP pension, giving a starting pension from age 60 of:

|

||||||||||||||||||||||||||||||||||||||||

|

Post-GMP equalization (assuming the member was male for the period 17th May 1990 to 5th April 1997), the pension at date of leaving is made up of the following component parts:

As the scheme only pays the GMP revaluation when the member reaches GMP age (60 for females but 65 for males), then for the benefits accrued in the period 17th May 1990 to 5th April 1997 the equivalent male member only receives statutory revaluation initially. This gives a lower starting pension from age 60 of:

|

||||||||||||||||||||||||||||||||||||||||

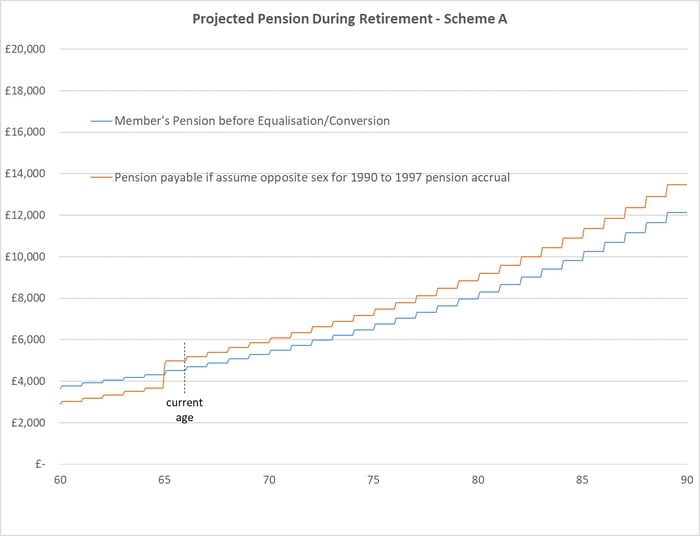

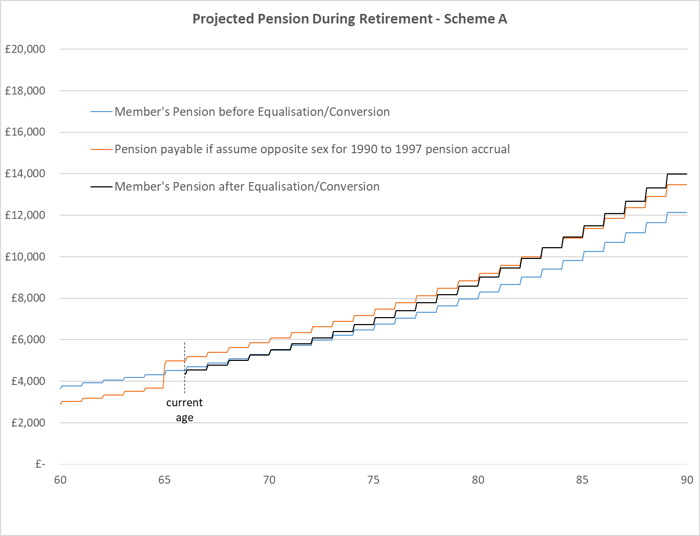

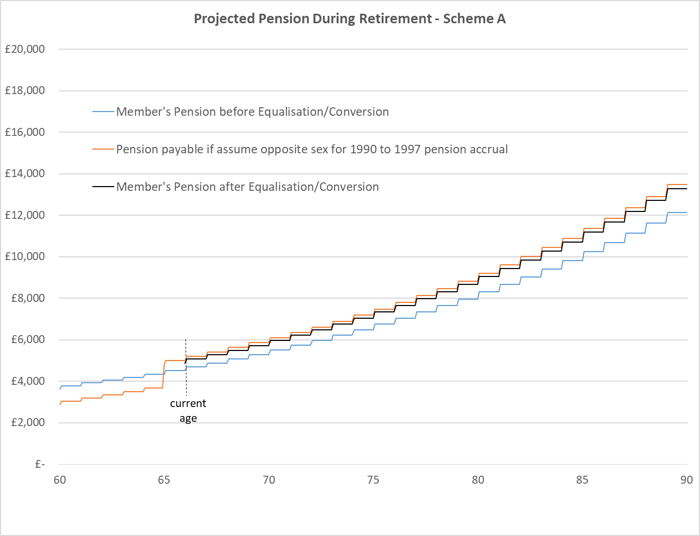

The pension cash flows for our female member and for the same member assuming opposite sex for the period between May 1990 and April 1997 are shown in the graphs below:

Looking at the two lines plotted above it is clear that, overall, the orange line represents the better option. Yes, there is an initial shortfall relative to the blue line, but the position switches at age 65 and a member with anything approaching average mortality would be better off adopting the pension income represented by the orange line. Therefore, the orange line represents the post-equalization pension that we need to value and convert.

The lines to the left of the ‘current age’ in the graph above represent the pension income received to date. Looking just at the amounts received to date, it is clear that the blue line represents the more favorable option in that Mrs. Atkins has received more to date than she would have if we had adopted the post-equalization pension from age 60. If the reverse were true, then we would expect the scheme to pay a lump sum payment to make good the historic shortfall. But we cannot expect Mrs. Atkins to repay the past overpayments. Instead, we will need to offset the value of these against the future value of the post-equalization pension.

Valuing the cash flows

Using the same valuation basis adopted in our previous blog, and rolling up past payments in line with bank base rates plus 1% (as per the DWP’s ‘Guidance on the use of the Guaranteed Minimum Pension (GMP) conversion legislation’) we have values before (Amount A) and after (Amount B) equalization of:

|

|

Amount A |

Amount B |

||

|

|

Past |

Future |

Past |

Future |

|

Scheme A |

£25,787.98 |

£166,888.34 |

£22,553.73 |

£185,045.20 |

This confirms what we concluded from the graph above—that overall, Amount B (the post-equalization option) is the more valuable. But, looking at the past payments in isolation, Mrs. Atkins has actually been paid more to date (£3,234.25 more including interest) than she would have received had the post-equalization pension been paid from age 60.

The total value of her future post-equalization/post-conversion pension should, therefore, equate to £185,045.20 less the £3,234.25 overpayments to date.

Converting values back into pension benefits

We have adopted a post-conversion pension with increases and spouse’s benefits in line with the scheme’s current practice for pre-97 excess benefits. This gives post-conversion benefits from the member’s current age (66) of:

|

|

Pre-97 Pension (5% p.a. increases) |

Post-97 Pension (5% p.a. increases) |

Total |

|

Scheme A |

£3,655.97 |

£676.88 |

£4,332.85 |

Adopting an alternative format for the converted pension benefits

However, Mrs. Atkins was already in receipt of the following pension at age 66:

|

|

GMP (CPI max 3% increases) |

Pre-97 Excess (5% p.a. increases) |

Post-97 Pension (5% p.a. increases) |

Total |

|

Scheme A |

£1,689.21 |

£2,140.64 |

£676.88 |

£4,506.73 |

The post-conversion benefit does represent an uplift in the value of her pension as the pre-97 benefits have removed GMP (which only increased at CPI, max 3% p.a.) in favour of a pre-97 pension that, while slightly lower to start with, does all increase at 5% p.a. The guidance dictates that for those who have already retired the post-conversion pension cannot be lower than the pension the member is currently receiving. However, the guidance does state that “if the benefits will be materially different in shape and form, the trustees may wish to consider giving members options.” One solution, therefore, would be to offer the member a post-conversion pension that contains an element of pre-97 pension increasing at CPI, max 3%. The following alternative post-conversion pension is equivalent in value but has a higher starting pension in exchange for lower increases on some of the pre-97 pension:

|

|

Pre-97 Pension (CPI max 3% increases) |

Pre-97 Excess (5% p.a. increases) |

Post-97 Pension (5% p.a. increases) |

Total |

|

Scheme A |

£1,689.21 |

£2,496.29 |

£676.88 |

£4,862.38 |

One would imagine that the above post-equalization/conversion pension would be acceptable to Mrs. Atkins. After all, the amount payable has stepped up from £4,506.73 to £4,862.38 and the part that receives the lower CPI, max 3% increase is unchanged, so the net increase is £355.61 p.a. increasing at 5% each year. This post-equalization/post-conversion enhancement has come at an estimated cost to the scheme of £14,923.43. In percentage terms, this represents an increase in the cost of providing Mrs. Atkins’s future pension of around 9%.

Death cases

We conclude by looking at a straightforward death case.

The first point to note is that, on death, any spouse’s GMP is payable immediately. This is true for both male and female members. The other point to note is that the statutory spouse’s GMP is 50% of the member’s GMP for all GMP accrual post 6 April 1988. This removes some of the larger inequalities we can encounter with retirement cases where the GMP is payable from different ages depending on gender.

The most common reason for inequality in our death cases will therefore simply be a result of the different proportion of GMP relative to pre-97 excess that results from female members accruing GMP at a faster rate than male counterparts.

|

As in our retirement example, the Pre-GMP equalization pension at date of leaving is made up of the following component parts:

The scheme adopts fixed-rate GMP revaluation along with statutory revaluation for non-GMP pension. The pension payable to the spouse on death before retirement is made up of the spouse’s GMP plus 50% of the non-GMP pension revalued to the date of death. Giving a starting spouse’s pension of:

|

||||||||||||||||||||||||||||||||||||||||

Let’s look again at Mrs. Atkins, but assume that instead of retiring at age 60 she died aged 58, at which point her husband received a spouse’s pension as follows:

|

As in our retirement example, the post-GMP equalization (assuming the member was male for the period 17th May 1990 to 5th April 1997) pension at date of leaving is made up of the following component parts:

The issue of different GMP payment ages for males and females does not apply here, as the spouse’s GMP is payable from date of death for both genders. So for the benefits accrued in the period 17th May 1990 to 5th April 1997 the male equivalent member passes on a very similar pension to their spouse. The difference arises simply as a result of the different split between the GMP and pre-97 excess, which in turn translates into a slightly different spouse’s pension as a result of the different revaluation applied to the GMP relative to that applied to the pre-97 excess between the date of leaving and date of death. This gives a marginally lower starting spouse’s pension of:

|

||||||||||||||||||||||||||||||||||||||||

One might conclude that there is no uplift required in this case, given that Mrs. Atkins’s spouse received a starting pension that was marginally higher than what he would have received had we assumed Mrs. Atkins was the opposite sex for her 1990 to 1997 accrual. But we must consider how the spouse’s pension inherited by Mr. Atkins will increase in payment during his lifetime. The GMP component will increase in line with CPI (max 3% p.a.) whereas the pre-97 excess and post-97 pension increases at 5% p.a. So, looking at the figures in blue in the two tables above, it is not difficult to see that the post-GMP equalization pension (although marginally less at the outset) is, in fact, the more valuable benefit as a larger proportion of the pension receives the higher 5% p.a. increases.

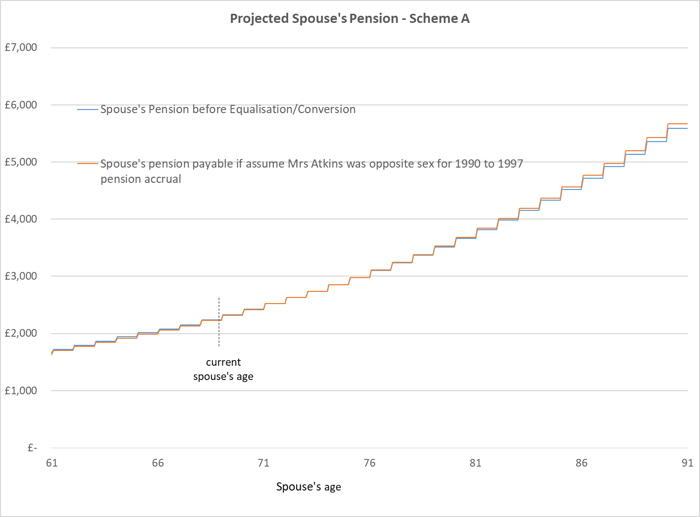

The pension cash flows for our spouse’s pension (and for the same spouse but assuming Mrs. Atkins was the opposite sex for the period between May 1990 and April 1997) are shown in the graphs below:

The differences are small, but we still need to go through the same process as we did for the retirement case.

Valuing the cash flows

We start by looking at the past payments, rolled up with bank base rates plus 1%. It’s hard to see from the graph above, but in the period up to the spouse’s current age, the blue line represents the higher cash flows. In other words, for the period from the date of Mrs. Atkins’s death to the current date, the spouse’s pension has been marginally higher than it would have been had we assumed Mrs. Atkins was the opposite sex for the 1990 to 1997 accrual. But as we progress forward, there will come a point when the reverse is true giving values before (Amount A) and after (Amount B) equalization of:

|

|

Amount A |

Amount B |

||

|

|

Past |

Future |

Past |

Future |

|

Scheme A |

£16,677.85 |

£68,756.08 |

£16,512.49 |

£69,277.04 |

Converting values back into pension benefits (adopting an alternative format for the converted pension benefits)

Again, the amount available to fund the post-conversion pension will be the higher of Amount A and B, less any past payments to date, i.e., £16,512.49 + £69,277.04 - £16,677.85 = £69,111.68. If we converted the available £69,111.68 into a pension increasing at 5% p.a., then the amount payable initially will be less than the current amount of the spouse’s pension inherited by Mr. Atkins. So we can provide the pension in two slices—one slice increasing at CPI, max 3% p.a. and the other increasing at 5% p.a.

This gives post-conversion benefits from the spouse’s current age (69) of:

|

|

Pre-97 Pension (CPI max 3% increases) |

Pre-97 Excess (5% p.a. increases) |

Post-97 Pension (5% p.a. increases) |

Total |

|

Scheme A |

£793.74 |

£1,107.96 |

£347.05 |

£2,248.75 |

The amount payable has stepped up from £2,238.35 and the part that receives the lower CPI max 3% increases is unchanged, so the net increase is £10.40 p.a. increasing at 5% each year.

In these blog posts, we have looked briefly at some examples of:

- Deferred members yet to retire

- Retirement at NRD (member still alive)

- Death before retirement (spouse still alive)

There are, of course, many other permutations to consider, including:

- Deferred members who have transferred out of the scheme

- Early and late retirements

- Retirements followed by death (spouse still alive)

- Retirements followed by death (spouse also died, before or after member)

- Death before retirement (followed by spouse’s death)

Of course, we have just looked at three example schemes throughout this blog and as we said at the beginning of this discussion, there is no such thing as a typical, defined benefit pension scheme.

There is also the small matter of gathering sufficient data to be able to recalculate benefits assuming the opposite sex for the 1990 to 1997 period. For example, you can imagine a scenario where a member retired early and subsequently died. You will undoubtedly have full details of the spouse’s pension currently in payment and full details of how each part increases in payment. But will you have readily available sufficient detail to enable you to go back and recalculate the benefits on a notional basis? You will need to recalculate the member’s early retirement pension assuming opposite sex for the 1990 to 1997 period, project that notional pension forward to determine the member’s pension amounts that would have been paid from the original retirement date, and calculate the spouse’s pension amounts that would have been paid from the member’s death

But whatever the scenario and whatever the scheme design, the process is similar:

- Calculate Amount A and Amount B using method C2 for past payments and method D2 for future payments.

- The amount available to fund the post-equalization/post-conversion pension is then the higher of Amount A and Amount B less the accumulated payments already received (rolled up with bank base rates plus 1%).

- Consider the format of the post-equalization/post-conversion benefits carefully so as not to reduce the pension currently in payment for those who are in receipt of their pension already. Ideally, adopt a format that is not dissimilar (in terms of increases and spouse’s proportions, etc.) to the pre-conversion pension format.

- If there are past shortfalls, then consider the payment of a lump sum—but only where it does not impede your ability to fulfill the requirement above.

.jpg)