BLOG. 4 min read

Retirement Income adoption trends by plan sponsors and participant utilization continued the strong momentum we saw during the first half of 2023. We agree with the recently released survey research from LIMRA, in-plan annuities and retirement income solutions are indeed at a tipping point.

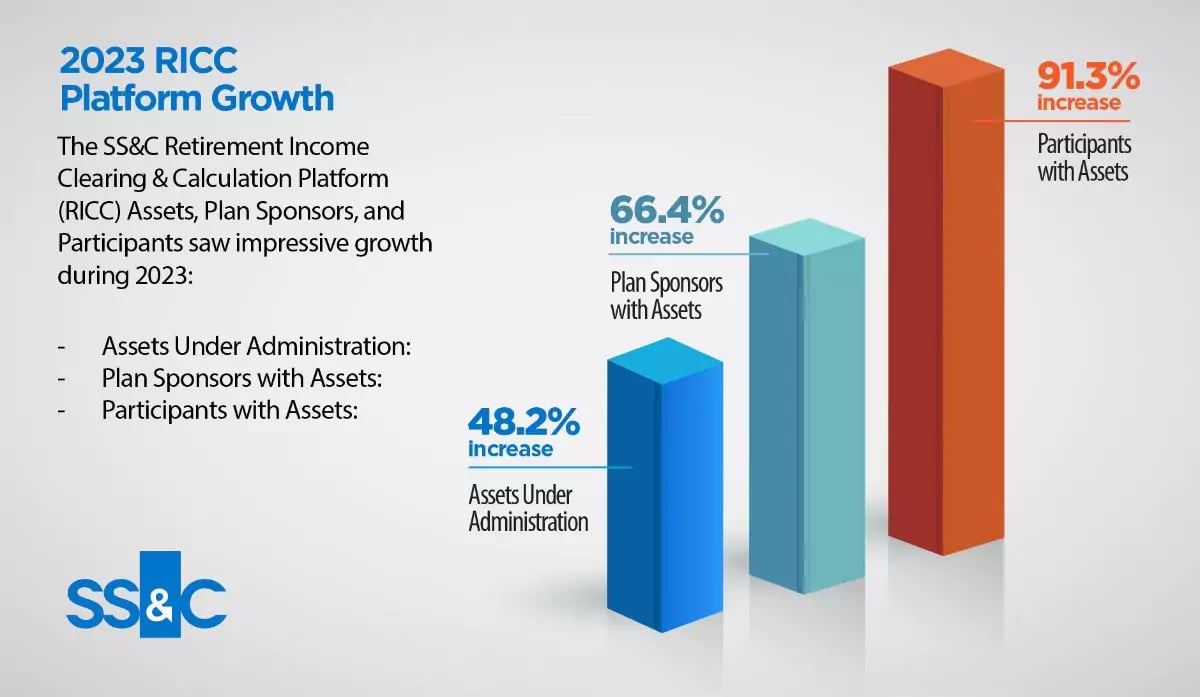

For our part, the SS&C Retirement Income Clearing & Calculation Platform (RICC) Assets, Plan Sponsors, and Participants saw impressive growth during 2023:

- Assets Under Administration: +48.19%

- Plan Sponsors with Assets: +66.35%

- Participants with Assets: +91.33%

The SS&C retirement income solutions team believes that 2024 will be an important year for retirement income. We will continue to work with our clients to provide efficient and scalable access to retirement income solutions, as plan sponsor implementations become increasingly focused on defaulting participants into solutions.

Retirement Income Access

Our team is still hearing some misleading messaging in the marketplace about the lack of interest or demand for retirement income solutions. Survey data shows that there is demand for retirement income solutions and that the demand is strong and growing. LIMRA’s survey research is some of the most recent to show strong demand for solutions from plan sponsors, with almost half of private sector plan sponsors with at least ten full-time employees considering adding a solution. Of these same plan sponsors, 75% will make a decision on product adoption within the next twelve months.

The real reason for the “slow uptake” of retirement income solutions is that the majority of these solutions are not widely available for use because recordkeepers do not currently offer them. Much like a retail product on a store shelf, retirement income solutions need to be connected and available on their recordkeeper’s investment menu. Once retirement income solutions are available at a recordkeeper, then a plan sponsor can implement and participants can allocate funds. The good news is that, in 2024, several recordkeepers are rolling out retirement income programs that will dramatically increase the products available to their plan sponsor clients and ultimately participants.

Legitimate consultant, advisor and plan sponsor portability concerns existed when the first retirement income products came to market. Fortunately, plans and participants now benefit from the SECURE 1.0 requirement that all retirement income solutions must provide product and benefit portability. The other good news is that, as recordkeepers roll out their retirement income programs, in most instances they are leveraging middleware and retirement income product technology networks to do so. Connected recordkeepers and connected products will benefit from the ability to port guaranteed benefits within the network, thereby providing the in-plan portability preferred by consultants, advisors, plan sponsors and participants.

Implementation as a Default

According to 2022 Cerulli data, 63% of assets flowing into 401k plans are landing in target date funds (TDFs), typically because these TDF solutions are implemented as the Qualified Default Investment Alternative (QDIA).[1] For retirement income solutions to capture a meaningful amount of asset flow and have a positive impact on plan participants that the industry intends, plan sponsors should consider implementing retirement income solutions as the default investment option.

QDIA is not the only default option available for plan sponsors to implement retirement income programs for their participants. Including an annuity or retirement income allocation within a managed account program is an option available to provide participants with a personalized level of allocation to guaranteed income, based on their needs and preferences. Paternalistic plan sponsors may also choose to allocate some or all of their employee’s profit sharing or 401k matching allocation to a retirement income solution. It was widely reported in November 2023 that IBM is ending their employee 401k match in favor of moving that match allocation to a guaranteed pension benefit, with a guaranteed interest amount. The IBM plan decision is one example of how plan sponsors can take a leadership role in providing retirement income solutions for their participants.

2024: An Important Year for Retirement Income Connectivity

As recordkeepers make their retirement income programs public, 2024 will be an important year as plan sponsors increasingly work with their recordkeeper and retirement income product partners to implement solutions. SS&C is excited about the opportunity to connect the defined contribution industry to retirement income solutions. This year we will see multiple large steps forward in transforming current supplemental savings plans into true retirement plans. These retirement plans will include retirement income solutions that will provide participants with the tools they need to turn their savings into retirement income.

To learn more about Retirement Income Solutions, visit our "Retirement Income Clearing & Calculation Platform (RICC®)" solution page or download our "Income Product Portability" brochure.

[1] Cerulli U.S. Defined Contribution Distribution 2023 report, Chapter 4 (Target-Date Funds: Product Development Trends and Innovation). Exhibit 4.02 historical data on 401(k) Target-date contributions as % of 401(k) contributions