BLOG. 8 min read

The Rise of ESG

The beginning of ESG investing is often set at 2006 and the establishment of the Principles for Responsible Investment (PRI), founded in 2006 by some of the world’s largest institutional investors with sponsorship from the United Nations.

Was there socially conscious investing prior to that? Sure. In the 1960s tobacco and apartheid were considered when making investments. The first socially conscious investment index was launched in 1990. (The 1990s also saw mutual “vice” funds.) But the UNPRI seemed to give ESG greater legitimacy and some semblance of industry structure. ESG investing, under its many labels, grew slowly but in recent years it has blossomed. Hard data on ESG is plentiful but much of that data is ambiguous.

So, how big is ESG investing?

This simple question is not so simple to answer. It depends on what is counted as ESG and who is counting. For example, PRI’s 2022 annual report includes the highlight, “… signatories total 4,902, with an estimated total of AUM of US$121.3 trillion.” That quote, though, must be read carefully because it touches on one of many ambiguities with ESG. Inside the AR reads, “PRI reports that the total AUM of all 4,902 signing entities is $121.3 trillion,” not that the total PRI AUM in ESG is $121.3 trillion. The consensus estimate of ESG AUM is generally believed to be between $2.5 trillion and $2.7 trillion, depending on mark to market date and who is reporting. For PRI to tout a $121.3 trillion headline figure that might be construed as ESG AUM is misleading. Data produced and/or analyzed by parties with vested interests in ESG like fund sponsors, rating agencies and consultants, data gathering companies largely tend to tell a favorable ESG story. By comparison, academic, and non-profit analyses tend to be more critical.

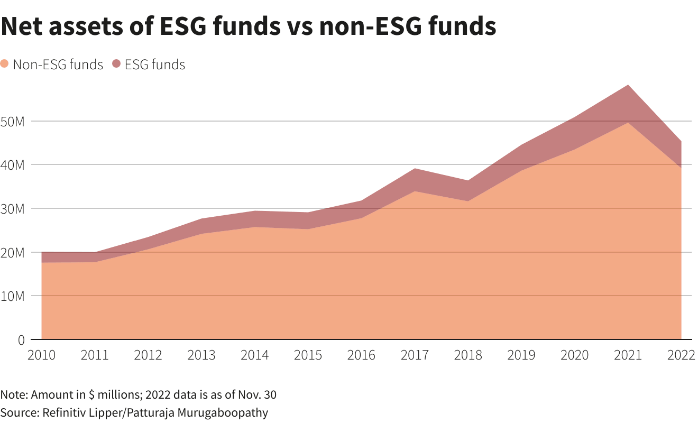

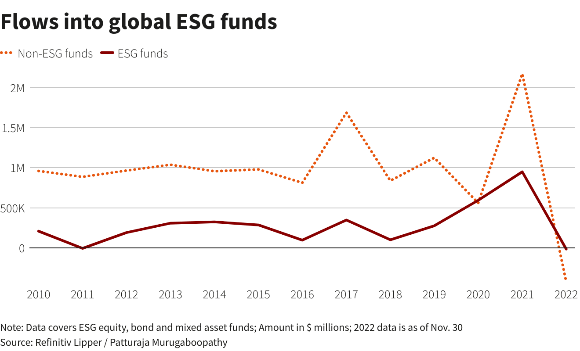

U.S. ESG as an asset class has seen sizeable growth in AUM. Funds increased ten-fold from $5 billion in 2018 to over $50 billion in 2020, then to nearly $70 billion in 2021 — the peak of ESG investing in the U.S. (Again, there is a range of values for U.S. ESG investment, depending on the source.) Total ESG funds were down 29% in 2022, compared to a 21% drop in non-ESG fund assets, reflecting declines in global stock and bond markets as central banks raised interest rates to reduce inflation, the Ukraine war, and political backlash against the industry. One of the largest U.S. funds, Parnassus Core Equity Fund, fell 26% in 2022, compared to a 19% decline of the S&P 500. Other major funds, like the iShares ESG Aware MSCI USA ETF and Vanguard ESG U.S. Stock ETF, saw similar declines of 20%+.

Global sustainable assets were approximately $2.5 trillion according to Morningstar. ($2.7 trillion per HBR). Only about 13% of these investment funds are U.S.-based and 81% are European-based.

How have ESG investments performed vis-à-vis non-ESG funds?

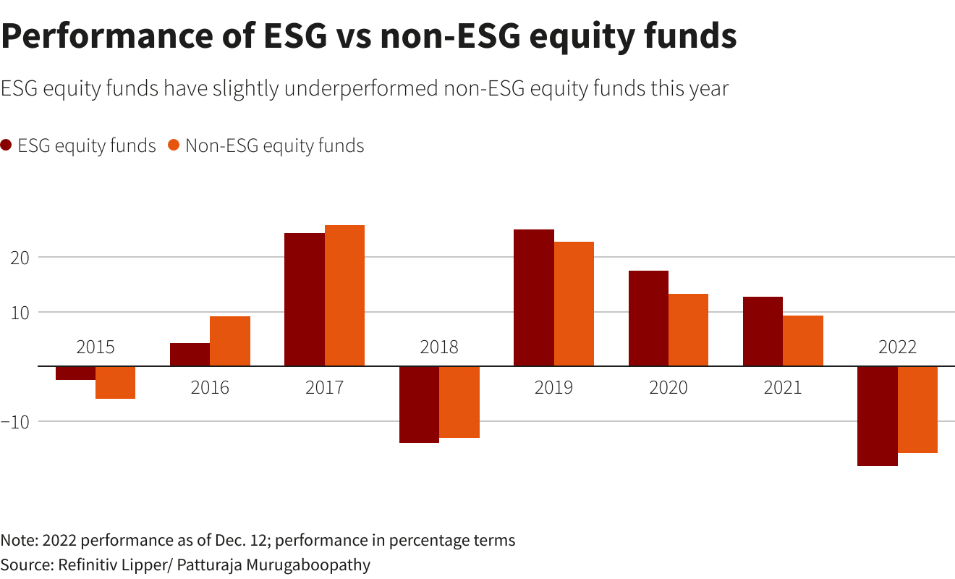

Evaluating the return performance of ESG investments is plagued by the previously referenced ambiguity problem. What is E or S or G? What metrics define an ESG fund? Such thorny issues will be examined in our upcoming blog post about the validity of ESG measurement. For the time being, this section uses ESG as commonly understood but loosely defined.

The most comprehensive meta-study of more than 1,000 research articles published between 2015-2020 reports 58% of those papers find a positive link between ESG and investment performance, while only 8% show a negative relationship, with the remaining 34% being neutral or mixed results.[1]

How have companies’ ESG activities performed before and after the adoption of ESG principles?

Not well it seems.

A Google search quickly identifies much data on ESG investment growth and strong ESG performance. Passing over the sponsored ads and those from entities with a vested interest in ESG (e.g., investment companies, rating agencies, data providers and ESG advocates) finds the following summaries of robust academic research:

- Columbia University and the London School of Economics compared the ESG record of U.S. companies in 147 ESG fund portfolios and that of U.S. companies in 2,428 non-ESG portfolios. They found the companies in the ESG portfolios had a worse compliance record for both labor and environmental rules. They also found that companies added to ESG portfolios did not subsequently improve compliance with labor or environmental regulations.[2]

- This is not an isolated finding. A European Corporate Governance Institute paper compared the ESG scores of companies invested in by 684 U.S. institutional investors that signed the UN’s PRI and 6,481 institutional investors that did not sign the PRI during 2013–2017. They did not detect any improvement in the ESG scores of companies subsequent to their signing PRI. Furthermore, the financial returns were lower and the risk higher for the PRI signatories.[3]

- University of Chicago researchers analyzed the Morningstar sustainability ratings of more than 20,000 mutual funds representing over $8 trillion of investor funds. Although the highest-rated sustainability funds attracted more capital than the lowest-rated funds, none of the high-sustainability funds outperformed any of the lowest-rated funds.[4]

How about companies’ PRI/ESG performance?

There is some evidence that companies publicly embrace ESG as a cover for poor business performance. Firms falling short of earnings expectations are more likely to cite stakeholder-focused objectives in their public communications around earnings announcements. This behavior suggests that managers push to be evaluated by subjective stakeholder-based performance criteria when falling short on objective shareholder-based measures.[5]

Finally, U.S. vs. non-U.S. performance

Analysis of companies that signed the PRI shows ESG performance materially differs between U.S. versus non-U.S. companies. While institutional investors located outside the U.S. improved their portfolio ESG scores by about 14% upon joining the PRI, there is no evidence that US PRI signatories do the same after signing the principles. The latter raises concerns about “greenwashing.”[6]

Conclusion

Debate on ESG and corporate social responsibility hinges on the assumption that good and bad companies can be defined confidently. That is not the case. Profitability and returns can be measured empirically but social responsibility is unspecific.

While there are some studies that find that companies that score high on the corporate responsibility scale reward investors with greater risk-adjusted returns, there is little evidence that socially responsible funds deliver excess returns. Socially responsible investing may be a noble cause but investors should not expect better returns as a result of it.

CPE Course Library | Are you curious to learn more about ESG Investing? Check out the GAMMA Library including over 300 hours of approved CPE courses including a course on ESG Investing as well as timely articles on the topic. Explore the full course listing, available CPE credits and registration for the GAMMA Library.

About Us | The SS&C Learning Institute is a division of SS&C dedicated to providing continuing education for today’s professionals. From a library of 250+ online CPE courses to microlearning articles and videos, our offerings are delivered by industry-leading subject matter experts and cover a wide variety of financial markets topics. To learn more about the SS&C Learning Institute, please visit ssctech.com/learn.

Monthly Newsletter | Subscribe to news from the SS&C Learning Institute to gain continued access to expert insights on the latest industry topics.

[1] Whelan, T., Atz, U., Clark, C., 2021. ESG and Financial Performance: Uncovering the Relationship by Aggregating Evidence from 1,000 Plus Studies. URL: https://www.stern.nyu.edu/sites/default/files/assets/documents/NYU-RAM_ESG-Paper_2021%20Rev_0.pdf.

[2] Do ESG Funds Make Stakeholder-Friendly Investments?

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3826357

[3] An Inconvenient Truth About ESG Investing, Harvard Business Review

https://hbr.org/2022/03/an-inconvenient-truth-about-esg-investing

[4] Do Investors Value Sustainability? A Natural Experiment Examining Ranking and Fund Flows https://doi.org/10.1111/jofi.12841

[5] Stakeholder Value: A Convenient Excuse for Underperforming Managers? https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3725828

[6] Do Responsible Investors Invest Responsibly? https://www.ecgi.global/working-paper/do-responsible-investors-invest-responsibly

%20(1).jpg)